By Aldo Santamaria | May 20, 2026

This P-Factor is typically not used as a base case or to size debt. It plays, however, a critical role in a specific lender stress test.

In the first blog post, P-Factors: What do P50, P75, and P99 mean in Project Finance? we explained how P-Factors translate uncertainty in renewable energy generation into cash flows. But not all P-Factors are used in the same way.

For example, P50 sits at the center of the distribution, and modelers frequently rely on it as a project’s base case. On the other hand, P99 lies on the lower end and represents a downside scenario. These two P-Factors are frequently used together (with their respective Debt Service Coverage Ratios) to size debt. We also mentioned P75, which represents a more cautious case, albeit not as extreme as P99.

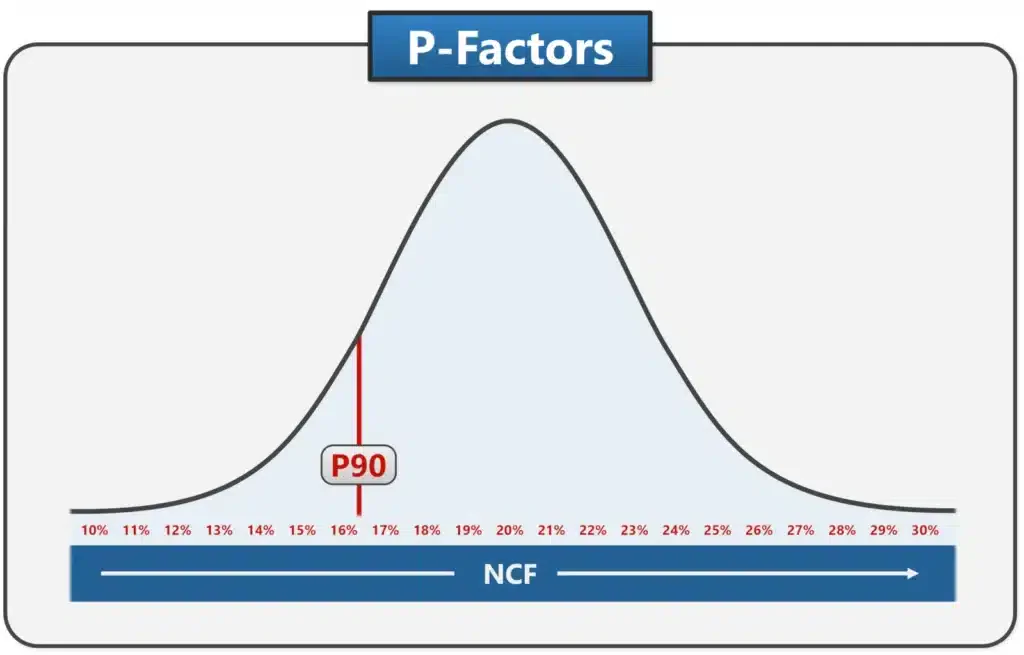

Now, there’s a particular P-Factor that tends to be used for a very specific purpose: P90. This one is typically not used as a base case, and in the United States, it is generally not used to size debt (although some practitioners will point out this is common in regions like Australia, Europe and parts of Asia).

Example of where P90 would sit in a normal distribution curve.

So, the question becomes: if we’re not using this P-Factor to size debt, why do lenders care about it?

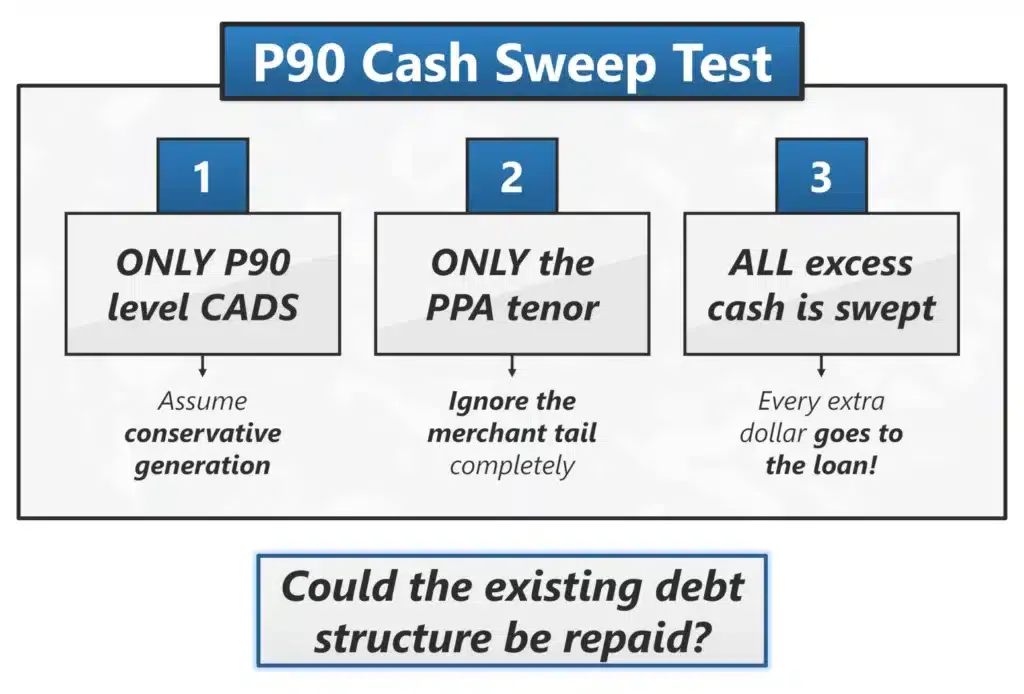

What is the P90 Cash Sweep Test?

When I first came across the test, I found out that some seasoned professionals even considered it a bit “weird”. I’m referring to the P90 Cash Sweep Test. And no, it’s not about cleaning up the model with a broom. A cash sweep simply means that, after repaying scheduled debt service, all excess cash goes to repay principal.

With that in mind, the test asks a hypothetical question:

Could the project repay its debt using only conservative, contracted cash flows, if every extra dollar were used to repay debt?

This isn’t about normal operations: it’s about lender confidence under constrained conditions. And more importantly, this test does not change the actual loan assumptions: it’s purely a hypothetical scenario used to evaluate the structure.

In practice, the test comes in two flavors:

- Version 1, focused on merchant tail risk

- Version 2, which incorporates refinancing risk through mini-perm structures

P90 Cash Sweep Test Version 1 (Merchant Tail Risk)

Imagine you’re a lender, and a developer is asking for a 20-year loan for a solar project. There is a Power Purchase Agreement (PPA) in place, which guarantees predictable revenues for the next 15 years. During the remaining 5 years, the project depends on merchant revenues.

As a lender, you naturally ask: How can I be sure I will get repaid?

This is exactly where Version 1 of the P90 Cash Sweep Test comes in: it checks if the deal can stand on contracted revenues alone. So, even though the project is not actually expected to operate in that way, lenders temporarily reframe the project under three assumptions:

- Use P90 CADS from contracted revenues instead of debt-case CADS.

- Limit CADS strictly to the PPA period (entirely excluding merchant revenues)

- Sweep all excess cash to repay principal

Then the question becomes: Can the full loan be repaid within the PPA period?

P90 Test: lenders temporarily reframe the project under three assumptions.

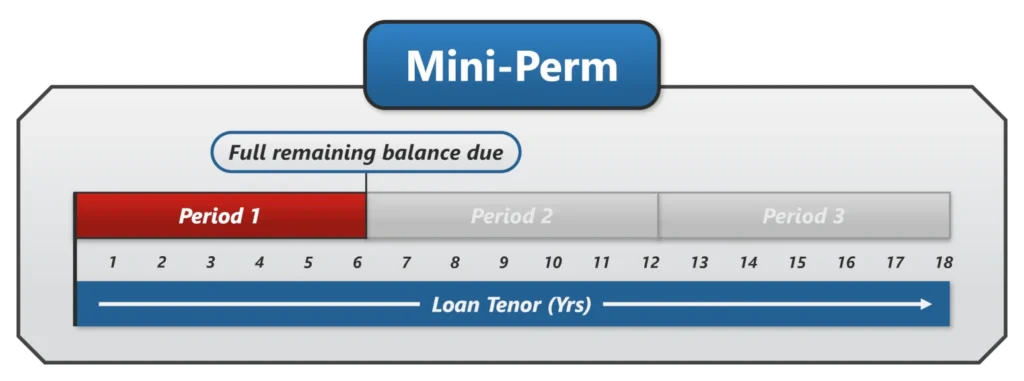

P90 Cash Sweep Test Version 2 (Mini-Perms)

The second version introduces an additional layer of complexity: refinancing risk. Here, we are dealing with mini-perm structures, where long-term debt is broken into shorter periods that require refinancing at intervals.

Mini-perms break long-term debt into shorter periods, each one having a balloon payment of the remaining balance at maturity.

For example, an 18-year loan might be structured as three 6-year tranches. Each one includes a balloon payment of the remaining balance at maturity. So, lenders are now exposed not only to merchant risk, but also to uncertainty in future financing conditions. This is where Version 2 of the test becomes relevant.

The main difference between Version 1 and Version 2 of the P90 Cash Sweep Test is timing. Instead of applying stress from day one, Version 2 splits the timeline:

- During the first period, apply base case CADS (just business as usual)

- The stress begins after the first refinancing (in our example, after year six)

From that point onward, lenders ask: If we assume conservative generation, remove the merchant tail, and redirect all excess cash to debt, can the remaining balance still be repaid within the remaining PPA period?

Final Thought: A Structure Test

You may be asking: what if the project fails the P90 test? This is a hypothetical scenario. It does not predict reality, nor does it assume the sweep will happen. Instead, it provides lenders with a reference point for evaluating the robustness of a project’s structure.

If the test fails, lenders do not necessarily walk away, but they may renegotiate, take a closer look at debt size and loan tenor, as well as require additional protection. In that sense, the P90 Cash Sweep Test is not about performance, but about structure under the inherent uncertainty that comes with renewable energy projects.

For readers looking to move from concept to application, Pivotal180 offers practical courses in Project Finance Modeling, as well as industry-specific programs covering areas such as battery storage and mining, with a focus on real-world deals.

Training with Pivotal180

We cover the P90 Cash Sweep Test topic in our advanced debt course and in the P-Factors mini course released in May 2026.

The Advanced Debt Course builds on our project finance modeling courses, including topics such as blended DSCR debt sizing, leverage constraints, P90 sweeps, junior debt, refinancing, and multi-tranche debt.

Pivotal180’s project finance modeling courses are designed to familiarize anyone, from analysts to the C-suite, with the knowledge and skills to build, analyze and communicate clearly about project finance models:

Course participants will learn how risk is allocated between lenders and sponsors, understand the structure and drivers of project finance transactions, and gain the necessary skills to run and evaluate operational or financing scenarios required to identify the most substantial risks and opportunities for any deal.

For readers looking to move from concept to application, Pivotal180 offers practical courses in Project Finance Modeling, as well as industry-specific programs covering areas such as battery storage and mining, with a focus on real-world deals.

Come model with us!